2026 SaaS Pricing Trends Driving Up Enterprise Costs

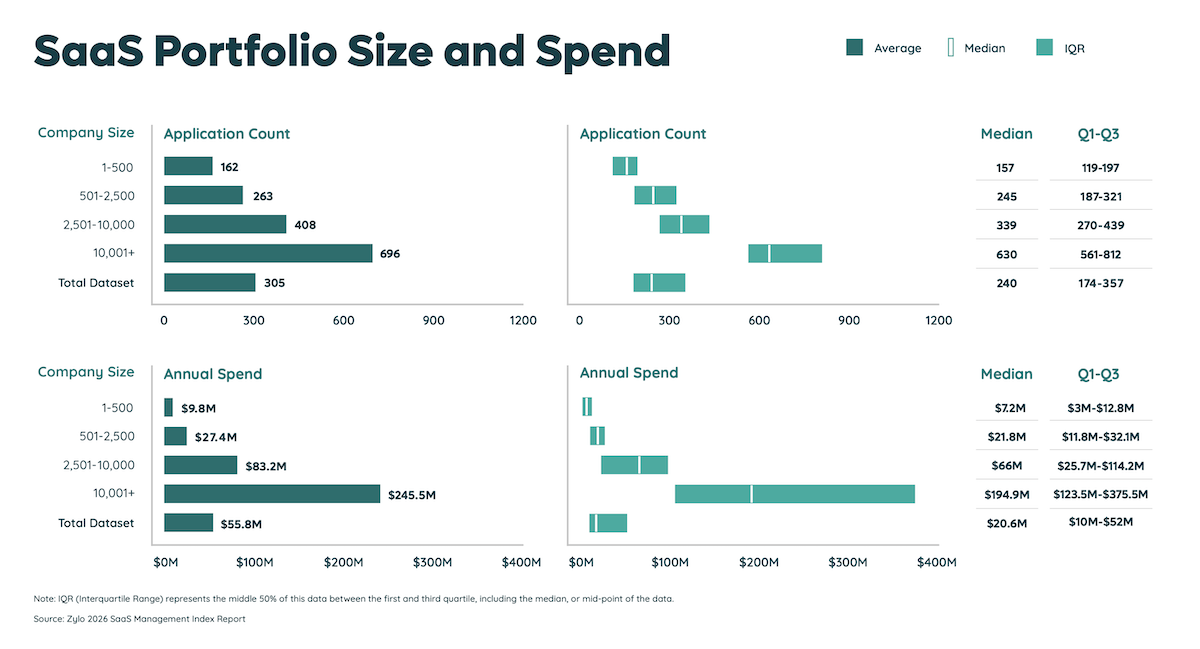

In 2025, organizations averaged 305 applications in their portfolio—according to Zylo’s 2026 SaaS Management Index. While that number remained relatively flat year over year, what did move was the bill. Spend rose nearly 8% in a single year, driven by how existing vendors are monetizing AI features, restructuring tiers, and layering consumption charges on top of subscriptions.

The financial impact is already forcing hard choices. Zylo’s survey of IT leaders found that 61% of organizations cut projects or initiatives because of unplanned SaaS cost increases in the past 12 months.

Budgets aren't failing because teams bought too many tools. They're failing because the tools they already own are getting more expensive in ways that annual planning cycles weren't built to absorb.

For Procurement and IT leaders, this shifts the challenge from controlling application sprawl to maintaining visibility into how software is priced, consumed, and renewed across an increasingly decentralized SaaS portfolio.

This article breaks down the five pricing trends reshaping enterprise SaaS economics in 2026, what each one looks like at the contract level, and what you can negotiate differently before your next renewal.

The Real Story Behind 2026 SaaS Pricing: Vendors Are Optimizing for Account Expansion

Customer acquisition has slowed across enterprise SaaS. If you've noticed your vendors getting more aggressive at renewal, more creative with bundling, or more insistent on multi-year commitments, there's a common thread: most vendors' 2026 revenue plans depend on extracting more from existing accounts rather than winning new ones.

That underlying pressure is the single force connecting every trend we’re discussing here. AI bundling, hybrid pricing, evergreen clauses, shorter terms, shrinkflation and opaque pricing pages: these are all variations of the same strategy, designed to grow average contract value within accounts that vendors already hold.

The pattern is visible across the software market. Vendors are increasing prices, introducing AI-powered editions, restructuring subscription tiers, and expanding consumption-based pricing. While the tactics vary, the objective is consistent: growing revenue within existing customer accounts rather than relying solely on new customer acquisition.

These moves all follow the same playbook. Gartner projects global software spending will reach $1.43T in 2026, a 15.1% year-over-year increase. That growth is coming from existing customers paying more per contract, per seat, and per unit of consumption.

Your job in 2026 is to recognize the pattern and negotiate against the strategy, not against any single tactic. That requires visibility into renewals, utilization, ownership, and contract terms across the portfolio so you can identify pricing risk early and respond with data rather than assumptions.

The SaaS predictions shaping 2026 reinforce this shift: as portfolios stabilize, the financial pressure is moving from sprawl to pricing mechanics.

SaaS Pricing Is Changing Faster Than Enterprise Budgets Can Keep Up

For most of the past decade, SaaS pricing was straightforward. You paid per seat, per month or per year, and the number on the invoice matched the number in your forecast. That predictability is disappearing.

Shifting Pricing Models

Vendors are moving away from static, seat-based subscriptions and toward variable pricing that fluctuates with usage, AI feature consumption, and tier restructuring. The result is a growing disconnect between annual budget cycles and the real-time consumption patterns that now drive a meaningful share of your software bill.

Artificial Intelligence

AI is accelerating that disconnect. Even when application counts remain relatively flat, software costs continue to rise as vendors introduce AI add-ons, consumption-based billing, and bundled tier upgrades. Organizations are increasingly managing the same number of applications at a higher cost per application.

The Business Impact of Volatile SaaS Pricing

The challenge is that these new pricing models operate on a different cadence than traditional budgeting. Finance teams plan around fixed entitlements and renewal schedules, while AI features, usage-based charges, and consumption meters can create costs throughout the contract lifecycle.

As a result, forecasting has become more difficult. By the time unexpected charges surface in a quarterly review, the spend is often already committed. This is one reason why SaaS cost volatility has become a growing concern for Procurement and IT leaders alike.

As pricing models become more dynamic, visibility becomes more valuable. When you can connect spend, usage, contracts, and renewals into a single operating model, your team is better equipped to identify cost drivers before they become budget problems.

Trend #1: SaaS Inflation Is Quietly Driving Up Costs

If you haven't benchmarked your renewal pricing against what you paid 12 months ago, start there. Renewal-time price increases have become the most reliable way vendors grow revenue from existing accounts, and most organizations don't catch the pattern until it's already compounded across the portfolio.

Zylo's 2026 SaaS Management Index found that 79% of IT leaders encountered price increases at renewal in the past 12 months. Renewal-time price increases have become the market default.

The increases show up in three forms:

- Straight renewal uplifts, where the vendor raises list price and applies it at your next contract cycle

- Bundled tier upgrades, where the features you're already using get promoted into a higher-priced plan and staying on the lower tier means losing functionality

- Mid-term price changes on variable components, where consumption-based line items adjust between billing cycles without triggering a formal renewal conversation

Costs Increase Without Additional Value

Cost per user is rising even when vendors aren't adding meaningful new capabilities to your plan. A Gartner analyst confirmed that SaaS subscription costs from several large vendors rose between 10% and 20% in 2025, outpacing IT budget growth projections of 2.8%. When your vendor raises prices 10% and your budget grows less than 3%, the math works against you every single renewal cycle.

Decentralized Purchasing Masks the Problem

The deeper problem is that most enterprises can't see the pattern forming. SaaS ownership is heavily decentralized: Zylo's data shows that lines of business control 81% of software spend while IT manages just 15%.

When dozens of teams manage their own renewals independently, nobody maintains the baseline comparison needed to spot a compounding uplift across 200+ contracts. If even a modest increase goes unchallenged on each renewal, the cumulative effect across the portfolio can be significant, and it's invisible without centralized tracking.

.png)

What to Negotiate Differently in 2026

- Lock your rate for the full contract term, including any renewal extension period. Vendors will often agree to a rate hold if you ask before signing, but rarely volunteer it.

- Cap annual uplifts contractually. A CPI-tied cap or a fixed ceiling of 5-7% gives you a predictable worst case instead of an open-ended exposure. If the vendor won't agree to a cap, that tells you something about their pricing trajectory.

- Protect variable components mid-term. If your contract includes any consumption-based line items, negotiate price protection on those rates for the duration of the agreement. A fixed per-seat rate means nothing if the per-token or per-API-call rate can change quarterly.

Negotiation is only part of the equation. Procurement teams need historical pricing data, renewal visibility, and license utilization insights to identify which vendors warrant scrutiny and where pricing increases can be challenged effectively. Without centralized visibility, incremental increases often go unnoticed until they accumulate across dozens of contracts.

Trend #2: AI and Usage-Based Pricing Are Introducing New Cost Variables

AI is reshaping how software vendors monetize existing products. Instead of relying solely on seat-based subscriptions, vendors are introducing credits, tokens, usage meters, AI add-ons, and bundled upgrades that create new cost drivers inside existing contracts. For Procurement and IT leaders, understanding these pricing mechanisms is becoming essential to forecasting spend and evaluating renewal proposals.

Features, Credits, Tokens, and Add-Ons

Start by auditing which vendors have added AI pricing on top of your current subscription. Many have, and the pricing structures vary enough that you can't apply a single forecasting model across your portfolio.

AI features are increasingly priced separately from base subscriptions, using credit-based, token-based, or per-action systems with conversion rates that aren't always transparent.

A few examples illustrate the range:

Microsoft Copilot

As of June 9, 2026, Microsoft 365 business plans include Copilot as a feature, which can range from roughly from $27 to $43 per user per month. Organizations that build custom AI experiences with Copilot Studio may also pay a $200 monthly platform fee that includes 25,000 messages, with additional usage driving further consumption-based costs. This combines subscription licensing, AI seat pricing, and metered consumption within a single ecosystem.

Salesforce Agentforce

On September 12, 2024, Salesforce announced the release of Agentforce, which started at $2 per conversation. In May 2025, it introduced Flex Credits at $0.10 per action and then added per-user licenses starting at $125 per user per month as a fast follow on June 17, 2025. Three pricing models for the same product in roughly 18 months.

Adobe Firefly

Adobe Firefly is bundled into Creative Cloud plans or individual Firefly plans with varying quantities of monthly generative credits for premium generation per user and unlimited access to standard generations. As of June 9, 2026, Firefly Pro costs $19.99 per month per license, while Premium is listed at $199.99 per month per license. The credit system uses variable consumption rates depending on the feature (generative fill costs more than a standard image generation). Credits reset monthly and don’t roll over. Users who consume their allotted credits can purchase a credit add-on plan.

Key Takeaway

While the mechanics differ, the underlying trend is consistent: software vendors are adding new pricing layers beyond the traditional per-seat subscription. Procurement teams evaluating renewals should assess both fixed licensing costs and variable consumption exposure.

Mandatory AI Bundling: The Hidden Price Increase

Watch for vendors moving AI features into existing tiers instead of selling them as optional add-ons. When AI capabilities get folded into the plan you're already on, the price goes up, and the "AI-free" option quietly disappears.

Several vendors, including Microsoft, have begun incorporating AI capabilities into broader suite pricing and packaging strategies.

The removal of lower-tier options is what makes this expensive. Once a vendor consolidates AI into standard plans and retires the older SKU, the ladder gets pulled up. You can't opt back into a plan without AI features because that plan no longer exists.

If you're approaching a renewal where AI bundling is on the table, push for AI-feature opt-out clauses that let you decline bundled capabilities you haven't adopted. Ask for audit rights on AI usage telemetry so you can see exactly what your organization is consuming before you're locked into a tier that assumes full adoption.

Why AI Pricing Breaks Traditional Budgeting

The challenge with AI pricing is visibility. Traditional licensing models make costs relatively easy to forecast because pricing is tied directly to user counts. AI pricing introduces additional variables that can change independently of headcount, including token consumption, credit usage, agent activity, and overage charges.

According to Zylo's 2026 SaaS Management Index, 78% of IT leaders experienced unexpected charges tied to consumption or AI features during the past year. In many cases, those costs emerged after contracts were signed and scaled faster than anticipated.

Now, Procurement and IT teams must extend SaaS Management beyond license counts and renewal dates. Monitoring consumption, adoption, and contract performance throughout the year is becoming equally important. Without that visibility, costs can increase long before a renewal conversation begins.

What to Negotiate Differently in 2026

- Set up consumption alerts at 50%, 75%, 90%, and 100% of any commit threshold. This gives your team lead time to adjust usage or escalate before overage charges hit.

- Negotiate AI-feature opt-out rights or split SKUs so you can adopt AI capabilities on your timeline rather than the vendor's bundling schedule. If a vendor insists on bundling, negotiate a price that reflects your actual adoption level rather than full-feature list pricing.

- Secure audit rights on AI usage telemetry, not just license counts. You need to see token consumption, credit usage, and per-user activity to forecast accurately and negotiate from a data-driven position.

- Cap overage rates contractually. Open-ended consumption charges are where budgets break. A reasonableness cap on per-unit overage pricing gives you a ceiling, even if usage exceeds your commitment.

The operational playbook for managing these costs is evolving alongside the pricing models. Consumption cost management is becoming a standalone discipline, and organizations that treat it as such will have a structural advantage at every renewal table. The SaaS predictions shaping 2026 point to this convergence of spend governance and AI adoption as one of the defining operational challenges of the year.

Trend #3: Hybrid Pricing Models Are Becoming the Default

If your vendor's latest renewal quote includes both a per-seat line item and a consumption-based component, you're already in a hybrid pricing model. And you're far from alone.

Hybrid pricing combines a fixed base license fee with variable costs tied to usage, consumption, or AI activity. The model has been standard in infrastructure (Snowflake, Databricks) for years, but it's now spreading across categories that were historically seat-based: CRM, collaboration, service management, and creative tools.

As vendors combine traditional subscriptions with consumption-based billing, hybrid pricing has expanded rapidly. Rather than replacing seat-based pricing, vendors are layering new charges on top of existing contracts, creating multiple cost drivers within a single agreement.

The shift is gaining momentum. The 2025 SaaS Benchmarks Report from High Alpha found that 42% of companies monetize AI features through usage-based or hybrid models, while Gartner projects that by 2027, 70% of leading SaaS vendors will offer consumption-based pricing across at least part of their portfolio.

Atlassian illustrates the shift toward hybrid pricing, combining subscription pricing, bundled AI entitlements, and consumption-based overages within a single contract.. As on June 9, 2026, standard plans include 25 Rovo AI credits per user per month, while products such as the Virtual Service Agency can generate additional charges of $0.30 per conversation when usage exceeds included limits.

Even vendors that haven't fully shifted are testing the waters: HubSpot now charges $10 per 1,000 AI credits beyond the allotment included in each subscription tier, and Zendesk prices its AI resolution agent at $1.50 per resolved conversation.

Per-seat pricing still accounts for the majority of enterprise SaaS spend, but the direction is clear. The contracts you negotiate in 2026 will increasingly carry both fixed and variable components, and your forecasting process needs to accommodate that. That means getting ongoing visibility into those patterns to avoid surprises and accurately model future spend.

Why Hybrid Pricing Makes SaaS Spend Harder to Control

Hybrid pricing introduces multiple cost drivers per tool, and each one behaves differently. That complexity is the core challenge.

Multiple Charges Apply to Individual Seats

A single application can now generate cost from the seat license, from AI credit consumption, from API call volume, and from storage or compute overages, all within the same contract. Finance teams that previously forecasted SaaS spend by multiplying seats by rate now need to model for seasonality, hiring plans, product launches, and department-level adoption curves, any of which can push the consumption component beyond budget.

Costs Are Incurred Between Billing Cycles

The timing makes it worse. Overages on consumption components often surface between billing cycles rather than at renewal. Zylo's survey of IT leaders found that 77% incurred unexpected costs after a contract was signed. In a hybrid model, this happens because the variable component behaves like a utility bill while the fixed component behaves like a subscription, and the two rarely align to the same review cadence.

Spend Accountability Suffers

Decentralized ownership compounds the problem. When software purchasing is spread across dozens of teams, and individual employees introduce roughly a third of all applications, the people driving consumption often aren't the people accountable for the budget. A marketing team running campaigns through an AI-enabled tool can generate meaningful overage charges without any visibility from the finance team that owns the forecast.

The operational gap is real. FinOps and ITAM teams are converging around shared responsibility for managing consumption-based SaaS, but most organizations haven't built the cross-functional workflows to monitor variable spend in real time. Until that infrastructure is in place, hidden overages will keep emerging between billing cycles.

What to Negotiate Differently in 2026

- Negotiate pooled commits across business units. If your vendor charges consumption-based fees, pooling your commit at the organizational level lets one team's underuse absorb another team's spike. This is especially valuable early in adoption when usage patterns are unpredictable.

- Push for true-down rights, not just true-ups. Most contracts allow you to add seats or credits mid-term if you exceed your commit. Far fewer let you reduce your commitment if consumption comes in lower than expected. True-down rights give you a contractual mechanism to right-size mid-term.

- Secure the rollover of unused commits into the next term. Credits, tokens, and consumption allotments that expire monthly or annually create a use-it-or-lose-it dynamic that benefits the vendor. Roll-over provisions let you carry unused capacity forward, which protects your investment and gives you more accurate data on actual consumption trends over time.

Hybrid pricing introduces complexity that many organizations are not structured to manage today. To adapt, you must treat SaaS as an operational category rather than a collection of individual vendor contracts, enabling better coordination between Procurement, IT, and Finance.

Trend #4: The Death of Grandfathered Pricing

For years, long-tenured customers could count on legacy pricing being honored at renewal. Loyalty discounts compounded, older SKUs stayed available, and vendors treated pricing stability as a retention tool. That era is ending.

Vendors are aggressively migrating customers off legacy plans, sunsetting older SKUs to force migration into modern (and more expensive) tiers, and unwinding the loyalty discounts that previously compounded at renewal. Three related shifts are driving this change:

- Legacy plan migrations are accelerating across the largest enterprise vendors

- Contract terms are getting shorter or more commitment-heavy, reducing buyer flexibility

- Public pricing pages are getting thinner, moving negotiation leverage back to the vendor

Each of these erodes a different layer of pricing predictability that buyers have relied on for years.

Legacy Plan Migrations

Review your current SKUs against each vendor's published product roadmap before your next renewal. If your plan is scheduled for retirement, you'll negotiate a better transition from a position of awareness than from a position of surprise.

The pattern is consistent across the biggest vendors in enterprise SaaS:

Microsoft

Microsoft is moving customers off legacy enterprise agreements as part of its July 2026 packaging update, bundling Copilot, Defender, and Intune capabilities into new suite structures that replace older commercial SKUs. Customers on legacy plans will see new pricing apply at their next renewal after July 1, 2026.

Atlassian

Atlassian has been executing the most aggressive migration in enterprise software. Server support ended entirely in February 2024. Then in September 2025, Atlassian announced full end of life for Data Center products by March 2029, with new Data Center purchases blocked for new customers as of March 30, 2026. Customers migrating from Data Center to Cloud can expect to pay roughly 28% more on average, and the ecosystem of Marketplace apps for Data Center is now frozen as of December 2025, with no new submissions accepted.

Salesforce

Salesforce raised prices 6% across Enterprise and Unlimited Editions in August 2025, following a 9% increase in 2023. At the same time, it retired standalone Einstein add-ons and Einstein 1 Editions, replacing them with bundled Agentforce plans that start at $125 per user per month. Customers on the old AI packaging are being moved into the new structure at renewal.

Adobe

Adobe restructured its AI offerings by separating the Firefly API from Creative Cloud into a standalone platform with its own pricing, credit system, and enterprise sales process. Legacy pricing guides no longer apply, and the old bundled model has been replaced by a tiered credit system where standalone Firefly plans exist separately from Creative Cloud subscriptions.

Shorter Terms, Bigger Commitments

Multi-year deals used to come with meaningful discounts that rewarded commitment. That calculus is changing in two directions simultaneously, and both favor the vendor.

On one side, vendors are pushing shorter terms. Twelve-month and quarterly contracts give vendors more frequent pricing resets. On the other, vendors are offering three-year prepay deals with minimum commits designed to lock in revenue.

Zylo's data captures the buyer-side response. Multi-year contracts grew from 23% of SaaS agreements to 38%, a 68% year-over-year increase. But the savings advantage of committing longer has nearly disappeared. Twelve-month contracts yield average savings of 16.4%, 24-month contracts 14%, and 36-month contracts 13%.

The gap between a one-year and a three-year deal is less than 3.5 percentage points. Organizations are locking in longer terms for predictability rather than discount, which means vendors are collecting commitment without giving up meaningful price concessions.

The two-direction split is itself a trend worth watching. Vendors with strong pricing power push shorter terms to capture more frequent uplifts. Vendors competing for retention push longer commits with minimum spend floors. Either way, the buyer's flexibility narrows.

The Return of "Contact Sales" Pricing

After a transparency wave between roughly 2018 and 2022, public pricing pages across enterprise SaaS are getting thinner. Vendors are pulling detailed pricing back behind sales conversations, which serves two purposes: it obscures AI-related uplifts, and it enables price discrimination between customers.

This is visible across the vendor examples already covered.

- Salesforce's Agentforce pricing page lists three consumption models but directs enterprises to contact sales for actual rates.

- Adobe's Firefly API requires an enterprise agreement with no published fixed rates; you negotiate based on volume.

- Microsoft's Copilot capacity packs and agent metering involve SCU allocations that vary by license tier and require rep-level conversations to model accurately.

For buyers, less public pricing means less leverage. When you can't point to a published rate card, benchmarking against peers becomes harder and the vendor controls more of the information asymmetry.

What to Negotiate Differently in 2026

- Negotiate migration credits when vendors sunset an SKU you're currently on, or a transition period that preserves your current pricing for a defined runway. A forced migration is leverage if you use it, because the vendor needs you on the new plan, and you can negotiate the terms of that move.

- Secure price holds for the remaining contract term regardless of what appears on the new pricing page. Your contract governs your rate, and a clause that explicitly decouples your pricing from future list-price changes protects you from mid-term surprises.

- Request long-tail support commitments for SKUs scheduled for retirement. If you're being asked to migrate, the vendor should guarantee support on your current plan through a reasonable transition window, not just through the end of the current billing cycle.

Trend #5: Hidden Pricing Changes Are Increasing (Shrinkflation in SaaS)

Price increases are easy to spot on an invoice. What's harder to catch is when the price stays the same but the value underneath it shrinks. That's shrinkflation in SaaS, and it's becoming one of the most effective ways vendors extract more from existing accounts without triggering the renewal-time scrutiny that a visible price increase would.

What Shrinkflation Looks Like in SaaS

Before your next renewal, pull your current plan's feature list and compare it line by line against the vendor's current pricing page. If the tier names or inclusions have changed since you signed, you may already be paying the same rate for less.

Shrinkflation takes three common forms:

- Feature removal at tier: capabilities included in your plan at signing are reclassified to a higher tier at renewal. You keep the same plan name and the same price, but accessing the same functionality now requires an upgrade.

- Reduced limits or quotas: API call caps, storage allotments, seat limits, and AI credit allocations quietly decrease within existing plans. Atlassian's Rovo credit system, for example, allocates 25 credits per user per month on Standard plans with overages possible on consumption features like the Virtual Service Agent. Adobe's Firefly credits reset monthly and don't roll over, and different features consume credits at different rates (generative fill costs more than a standard image generation). Credits reset monthly and don't roll over.

- Restructuring that promotes existing features into higher plans: When a vendor reorganizes its packaging and your current features land in a more expensive tier, the result is a price increase that doesn't show up as one. Microsoft's July 2026 pricing update bundles Copilot Chat, Defender, and Intune capabilities into existing suite tiers while raising the list price of those tiers. If you already purchased Defender or Intune as standalone add-ons, you may save on the bundle, but if you didn't need those features, you're absorbing their cost anyway.

Why SaaS Contract Changes Go Unnoticed

Shrinkflation thrives in environments where nobody owns the full picture. Most organizations lack the centralized tracking needed to compare what was included in a plan at signing against what that same plan includes 18 months later, and the reasons come down to how SaaS is bought, managed, and renewed.

Decentralized buying is the primary driver. When lines of business control 81.1% of spend and IT manages just 15.2%, renewal ownership is scattered across dozens of teams. The marketing team renewing its creative tools doesn't cross-reference the plan inclusions against what was signed two years ago. The engineering team renewing its project management suite doesn't check whether its API limits have changed since the last contract. Each team manages its own renewals in isolation, and none of them holds the institutional baseline that would surface a packaging change.

Three gaps make the problem worse:

- No baseline comparison documents. Few teams keep a record of exactly what was included in each tier at signing, which means there's no reference point to measure against when the vendor restructures packaging mid-contract or at renewal.

- Poor renewal visibility. With an average of 211 renewals per year, that's nearly one per business day. Many teams don't review the current pricing page until they're already mid-negotiation, which means the shrinkflation has already been accepted as the starting position.

- Renewals treated as administrative checkpoints. Only 38.1% of IT leaders in Zylo's survey consider renewals a key opportunity to reduce software costs, which means the majority are rubber-stamping rather than scrutinizing what they're getting for the price.

The cumulative effect is significant. Organizations carry an average of $19.8M in annual license waste, and a meaningful share of that waste comes from paying for tiers, features, and quotas that no longer match actual usage, often because the plan structure shifted underneath the contract without anyone flagging it.

What to Negotiate Differently in 2026

- Secure feature-parity guarantees for the full contract term. A clause that locks the features included in your tier at the time of signing protects you from mid-term restructuring. If the vendor reorganizes its plans during your contract, you keep access to everything you originally purchased at the rate you originally agreed to.

- Add quota-protection clauses on existing tiers. If your contract includes API limits, storage caps, or credit allotments, those limits should be contractually fixed for the term. A vendor should not be able to reduce your allocation without triggering a renegotiation or a pricing adjustment in your favor.

- Negotiate notification rights when tier definitions change. Even if a feature-parity clause protects your current term, you need advance notice of any packaging changes that will affect your next renewal. A 90-day notification requirement gives your team time to evaluate the impact and prepare a negotiation strategy rather than discovering the change mid-cycle.

What's NOT Changing in 2026 SaaS Pricing

The trends above are real and accelerating, but context matters. Understanding where the conventional wisdom overstates the change is just as useful as tracking where it understates it.

In 2026, per-seat pricing will continue to dominate, renewals will remain a key cost-saving lever, and full AI monetization will still be the exception.

Per-Seat Pricing Still Dominates

Despite the noise around consumption and hybrid models, the 2025 SaaS Benchmarks Report from High Alpha found that 53% of companies still monetize exclusively through subscription models, and only 42% have moved to usage-based or hybrid approaches. The shift is real, but seat-based pricing remains the predominant way enterprises pay for software in 2026.

Negotiation Leverage Still Exists at Renewal

Most enterprise renewals still close within a manageable range for buyers who actually negotiate. Zylo's data shows that organizations achieve average savings of 16.8% at renewal, with even higher returns on 12-month contracts (16.4% average savings). The leverage exists. The problem is that only 38% of IT leaders treat renewals as a cost-reduction opportunity, which means the majority are leaving savings on the table through process gaps rather than a lack of negotiating power.

Full AI Monetization Is Still the Exception

The "AI is everything" narrative also tends to outrun reality. While vendor pricing pages and earnings calls emphasize AI, only a fraction of most vendor catalogs have fully shifted to AI-bundled pricing. The High Alpha data shows that among companies with AI features in their product, 26% aren't monetizing them at all, and another 33% are still in the testing phase. Full AI monetization is concentrated among the largest platform vendors. For the long tail of your SaaS portfolio, the renewal you're preparing for probably still looks a lot like last year's.

What This Means for Your 2026 Strategy

None of this diminishes the urgency of preparing for hybrid, consumption, and AI-driven pricing. Panicking into sweeping process changes across every contract isn't the right response either. Focus your new playbook on the vendors and contracts where the pricing model has actually changed, and apply your proven renewal discipline to the rest.

How Enterprises Can Regain Control of SaaS Pricing

The trends above share a common denominator: they reward organizations with visibility, process, and leverage, and they punish organizations that manage renewals reactively. Regaining control means building the operational infrastructure to see, optimize, and negotiate across both fixed and variable cost structures.

Build Visibility Across Fixed and Variable Costs

Start with a complete picture of what you're actually spending, across both subscription and consumption models, in a single view. Most organizations can't produce this today because their SaaS data lives in separate systems:

- Contract management tracks subscription terms

- Finance systems capture invoice-level spend

- Consumption data sits in vendor-specific dashboards that nobody outside the technical team monitors

Use discovery to bring financial data together.

SaaS discovery surfaces shadow IT and hidden spend across expense feeds, SSO logs, and finance systems so you can see the full portfolio before you start optimizing it. Zylo's data shows that 3.67% of SaaS spend and 45.3% of applications are purchased through expense channels, and ChatGPT is now the most expensed application by transaction count. You can't control spend you can't see, and expense-based purchasing is the fastest-growing blind spot.

Build predictive budgeting around leading indicators rather than trailing finance reports. Historical spend data tells you what happened. Usage trends, consumption patterns, and upcoming renewal timelines tell you what's about to happen. In a pricing environment defined by variability, the organizations that forecast forward will outperform the ones that reconcile backward.

Optimize Licenses and Eliminate Waste

Visibility alone doesn't reduce spend. Once you can see the full portfolio, the next step is systematically identifying where you're paying for more than you're using and acting on it before the next renewal.

- Reclaim unused seats systematically before every renewal. Organizations use just 54% of their SaaS licenses on average, which translates to $19.8M in annual license waste. That waste represents direct savings available at renewal, because every unused seat you reclaim before renegotiation reduces the baseline the vendor prices against.

- Identify redundant tools and consolidate vendor count. With hundresds of applications in the portfolio, overlap is inevitable. The three most redundant application categories are online training, team collaboration, and (for the first time) generative AI. Every redundant application is a consolidation opportunity that reduces both licensing cost and management overhead.

- Right-size tiers to actual usage rather than aspirational usage. If your team purchased Premium licenses for capabilities that only 30% of users access, that's an optimization opportunity. Downgrading to a lower tier and purchasing add-ons only for the users who need them often produces a lower total cost than maintaining a uniform tier across the full user base.

Prevent Consumption Cost Overages

Monitor consumption costs on a regular cadence, not just at renewal. In a hybrid or usage-based model, overages emerge between billing cycles, and costs can spike as frequently as daily or weekly, depending on the pricing model. Waiting for the next renewal to address them means absorbing weeks or months of unplanned spend.

Set alerts to detect anomalies, spending spikes, and threshold breaches against your commit. If your contract includes a consumption commit, you should know when you've crossed 50%, 75%, and 90% of that commit, not when you receive the overage invoice.

Continuously forecast your spending commitments. Understanding whether you're trending toward full utilization, underuse (wasted commit), or overuse (overage exposure) lets you adjust mid-term rather than reacting at renewal.

The Contract Clauses to Negotiate in 2026 (Consolidated Checklist)

Every negotiation tactic from the trend sections above rolls up into a single set of contract provisions. This is the checklist your procurement and IT teams should carry into every renewal conversation this year:

- Rate lock for the full term, including any renewal extension

- Annual uplift cap (CPI-tied or 5-7%)

- AI-feature opt-out rights or split SKUs

- Consumption alerts at 50/75/90/100% of commit

- Audit rights on AI usage telemetry

- True-down rights, not just true-ups

- Roll-over of unused commits into the next term

- Pooled commits across business units

- Migration credits when SKUs are sunsetted

- Feature-parity guarantees for the contract term

- Quota-protection clauses

- Termination-for-convenience on consumption components

- Extended notice periods (or removal of evergreen auto-renewal)

Not every clause will apply to every contract, but every contract should be evaluated against this list. The vendors with the most complex pricing structures are the ones where the most clauses will be relevant.

Organizations that are still reacting to pricing changes rather than proactively controlling costs will continue to lose ground. Those who build this checklist into their standard renewal workflow will negotiate from a structurally stronger position on every deal.

How Zylo Helps Enterprises Manage SaaS Pricing in 2026

Every trend in this article points to the same operational requirement: you need complete visibility into what you're spending, how it's being consumed, and when you have leverage to change the terms.

The result is less waste, fewer overages, and complete financial control across your SaaS portfolio. Whether you're preparing for renewals shaped by AI bundling, tracking consumption-based spend, or building the benchmarking foundation to negotiate the contract clauses, Zylo gives your team the visibility and leverage to act.

Learn how Zylo helps IT, SAM, Procurement, and FinOps teams control SaaS and AI costs, save money, and reinvest in the business. Request a demo to see it in action.